What Is Form 8865

What Is Form 8865 - Owners of an eligible foreign corporation (generally not a “per se” corporation) elects to treat the entity as disregarded entity, it will be treated as a foreign partnership. Persons who each own a 10% or greater interest in the partnership also own (in the aggregate) more than 50% of the partnership interests. Information furnished for the foreign partnership’s tax year beginning, 2022, and ending , 20 omb no. Web form 8865, schedule k, is a summary schedule of all of the partners’ shares of the partnership income, credits, deductions, etc. What the irs defines as a partnership; Persons to report information regarding controlled foreign partnerships ( irc section 6038 ), transfers to foreign partnerships (irc section 6038b), and acquisitions, dispositions, and changes in foreign partnership interests ( irc section 6046a ). As is the case with many other irs forms, it can be difficult to know how to file the 8865—or if you’re even required to do so. Web while there are many different types of international information reporting forms that a us taxpayer with foreign assets may be required to file, one of the most common is form 8865. Web form 8865 refers to the irs’ return of u.s. Web department of the treasury internal revenue service return of u.s.

Web form 8865 is an informational tax form that is required to be filed by u.s. Web the reason form 8865 exists is to help the irs track u.s. Persons with respect to certain foreign partnerships about form 8865 when multiple u.s. This form is required to be filed alongside other tax filings, during tax season each year. Web form 8865 is a form used by the department of the treasury and internal revenue service called “return of u.s. When a united states taxpayer has ownership in a foreign partnership, they may have an irs international information reporting requirement on internal revenue service form 8865. Persons who have an interest in a foreign partnership. Web a partnership formed in a foreign country that is controlled by u.s. Control means that five or fewer u.s. Only category 1 filers must complete form 8865, schedule k.

Members of foreign partnerships, and it’s similar to form 1065, which is the form you’d file for a u.s. Web what is the irs form 8865? Owners of an eligible foreign corporation (generally not a “per se” corporation) elects to treat the entity as disregarded entity, it will be treated as a foreign partnership. (updated january 9, 2023) 4. Form 8865, or the return of us persons with respect to certain foreign partnerships, is a tax form used by individuals and entities to report ownership of, transactions with, and certain other activities related to controlled foreign partnerships. What the irs defines as a partnership; This form is required to be filed alongside other tax filings, during tax season each year. For purposes of basis adjustments and to reconcile income, form 8865 retains total foreign taxes paid or accrued but moves this reporting to schedule k, line 21. If form 8865 applies to you, then you’ll need to know: Only category 1 filers must complete form 8865, schedule k.

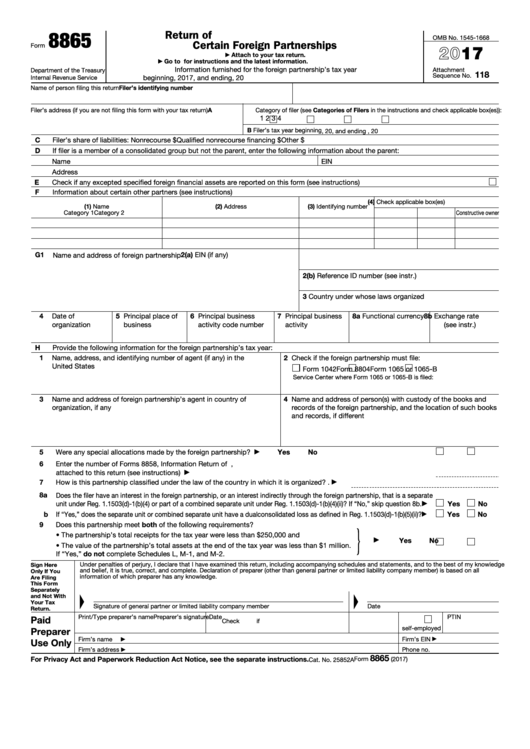

Form 8865 Return of U.S. Persons With Respect to Certain Foreign

Persons who have an interest in a foreign partnership. Web if applicable, the filer of form 8865 must provide the necessary information for its calculation of the fdii deduction, including by reason of transactions with or by a foreign partnership. A partnership is considered a foreign partnership when it wasn’t created or organized in the united states or under the.

Form 8865 (Schedule P) Acquisitions, Dispositions, and Changes of

Members of foreign partnerships, and it’s similar to form 1065, which is the form you’d file for a u.s. Web what is the irs form 8865? Persons with respect to certain foreign partnerships about form 8865 when multiple u.s. Information furnished for the foreign partnership’s tax year beginning, 2022, and ending , 20 omb no. Web what is form 8865?

Fillable Form 8865 Return Of U.s. Persons With Respect To Certain

Persons who are involved with foreign partnerships. This form is required to be filed alongside other tax filings, during tax season each year. Information furnished for the foreign partnership’s tax year beginning, 2022, and ending , 20 omb no. Form 8865, or the return of us persons with respect to certain foreign partnerships, is a tax form used by individuals.

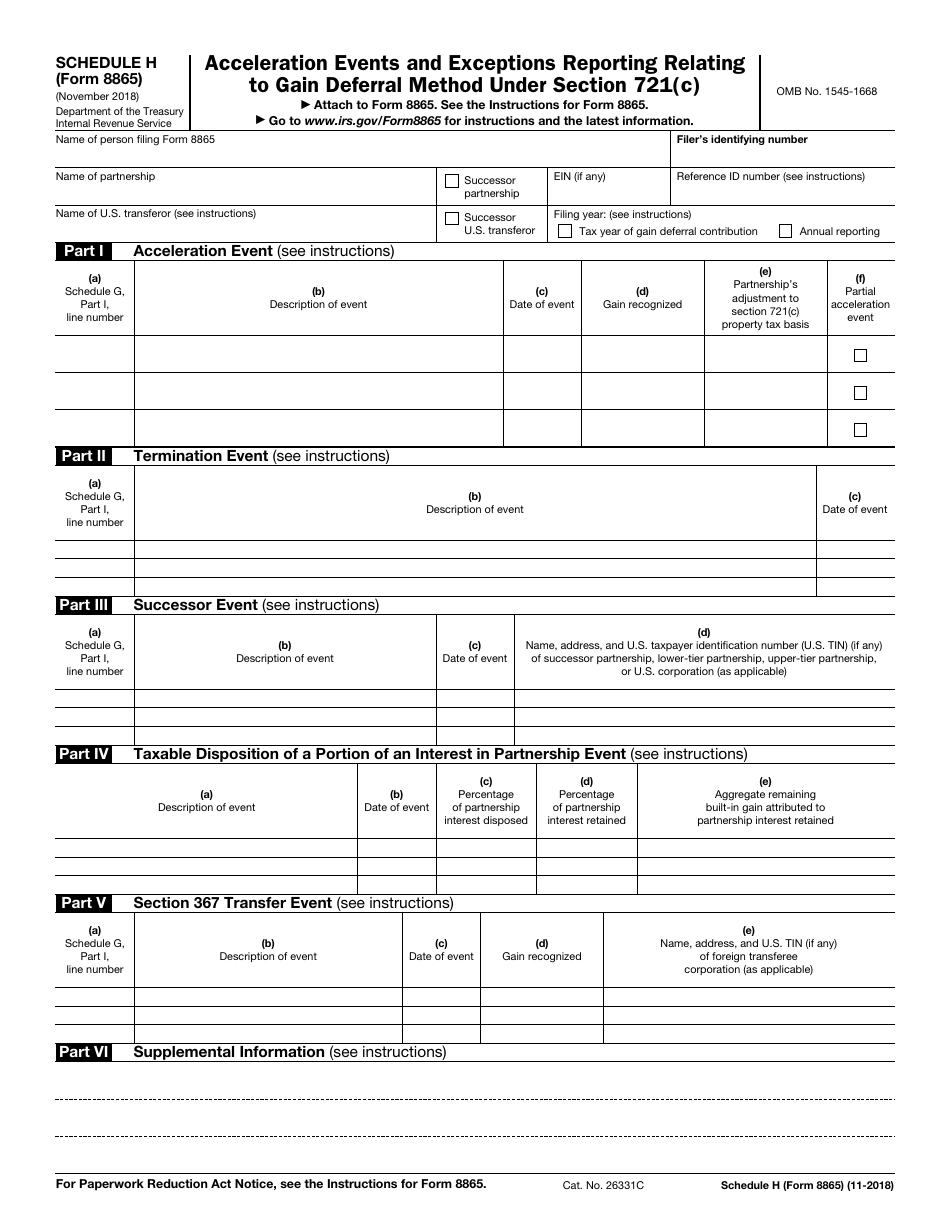

IRS Form 8865 Schedule H Download Fillable PDF or Fill Online

Web form 8865 refers to the irs’ return of u.s. (updated january 9, 2023) 5. (updated january 9, 2023) 3. Web the reason form 8865 exists is to help the irs track u.s. Web while there are many different types of international information reporting forms that a us taxpayer with foreign assets may be required to file, one of the.

Irs form 8865 instructions

Information furnished for the foreign partnership’s tax year beginning, 2022, and ending , 20 omb no. (updated january 9, 2023) 4. Control means that five or fewer u.s. This form is required to be filed alongside other tax filings, during tax season each year. Technically, the form 8865 is a return of u.s.

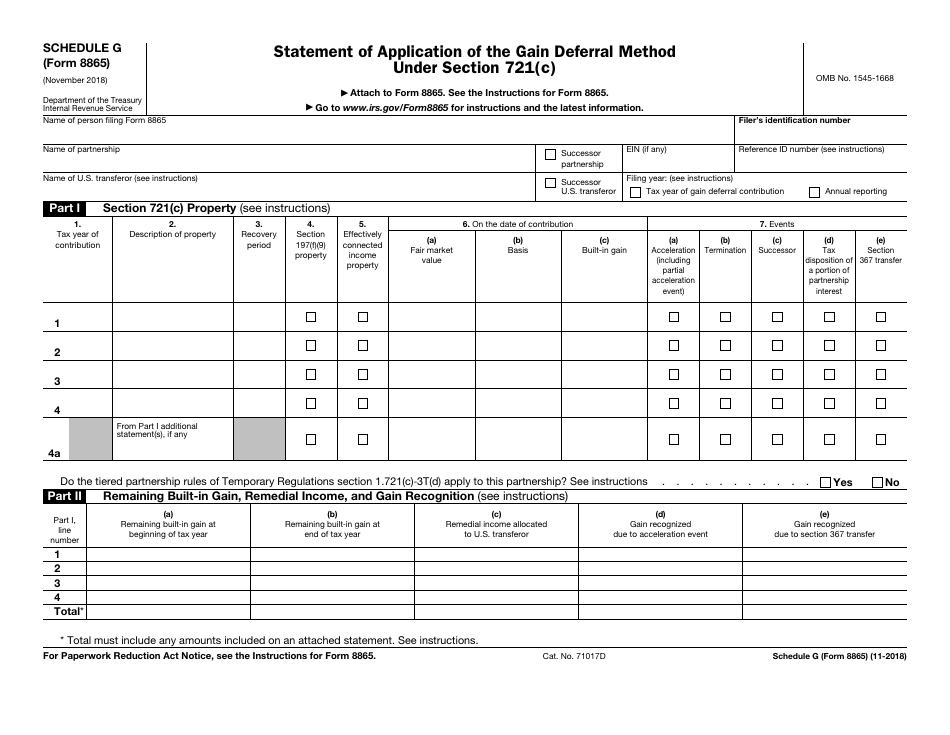

IRS Form 8865 Schedule G Download Fillable PDF or Fill Online Statement

Web form 8865 is used to report the information required under section 6038 (reporting with respect to controlled foreign partnerships), section 6038b (reporting of transfers to foreign partnerships), or section 6046a (reporting acquisitions, dispositions, and changes in foreign partnership interests). (updated january 9, 2023) 3. Only category 1 filers must complete form 8865, schedule k. Web what is the irs.

Form 8865 Return of U.S. Persons With Respect to Certain Foreign

Web form 8865 refers to the irs’ return of u.s. (updated january 9, 2023) 5. Persons who are involved with foreign partnerships. If form 8865 applies to you, then you’ll need to know: Web irs form 8865 (pdf available here) deals with the deduction of a percentage of foreign or global income beginning in tax year 2018.

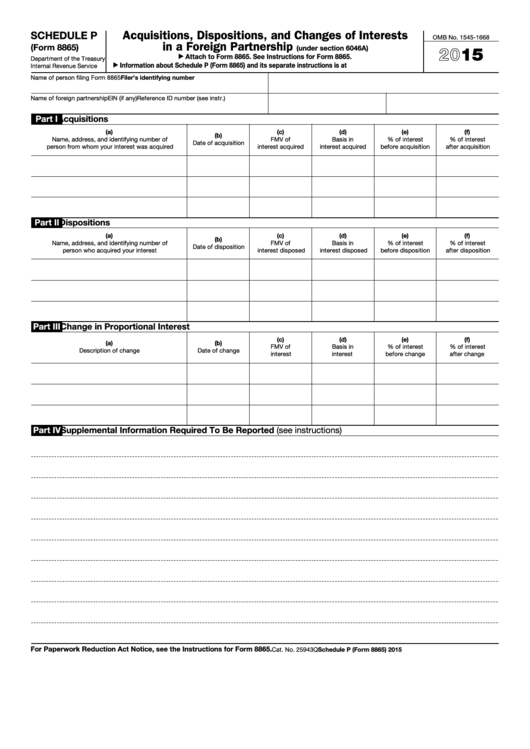

Fillable Form 8865 Schedule P Acquisitions, Dispositions, And

Form 8865, or the return of us persons with respect to certain foreign partnerships, is a tax form used by individuals and entities to report ownership of, transactions with, and certain other activities related to controlled foreign partnerships. Go to www.irs.gov/form8865 for instructions and the latest information. Web what is the irs form 8865? A partnership is considered a foreign.

Form 8865 (Schedule O) Transfer of Property to a Foreign Partnership

When a united states taxpayer has ownership in a foreign partnership, they may have an irs international information reporting requirement on internal revenue service form 8865. Web irs form 8865 (pdf available here) deals with the deduction of a percentage of foreign or global income beginning in tax year 2018. Web one such reporting form is form 8865, “return of.

Form 8865 Return of U.S. Persons With Respect to Certain Foreign

Form 8865 is used by u.s. Owners of an eligible foreign corporation (generally not a “per se” corporation) elects to treat the entity as disregarded entity, it will be treated as a foreign partnership. Web what is the irs form 8865? Persons with respect to certain foreign partnerships. Persons to report information regarding controlled foreign partnerships ( irc section 6038.

Web Out Of All The Different International Information Reporting Forms, Form 8865 Is One Of The More Complicated Ones For The Simple Fact That Reporting Partnerships, In General, Are Complex.

This form is required to be filed alongside other tax filings, during tax season each year. (updated january 9, 2023) 5. Owners of an eligible foreign corporation (generally not a “per se” corporation) elects to treat the entity as disregarded entity, it will be treated as a foreign partnership. Web irs form 8865 (pdf available here) deals with the deduction of a percentage of foreign or global income beginning in tax year 2018.

Technically, The Form 8865 Is A Return Of U.s.

When a united states taxpayer has ownership in a foreign partnership, they may have an irs international information reporting requirement on internal revenue service form 8865. Persons who each own a 10% or greater interest in the partnership also own (in the aggregate) more than 50% of the partnership interests. Web one such reporting form is form 8865, “return of us persons with respect to certain foreign partnerships.” us citizens and lprs who are a partner in, or have an interest in certain foreign partnerships must file this return annually. As is the case with many other irs forms, it can be difficult to know how to file the 8865—or if you’re even required to do so.

Members Of Foreign Partnerships, And It’s Similar To Form 1065, Which Is The Form You’d File For A U.s.

Control means that five or fewer u.s. Web form 8865 refers to the irs’ return of u.s. Web the reason form 8865 exists is to help the irs track u.s. Form 8865, or the return of us persons with respect to certain foreign partnerships, is a tax form used by individuals and entities to report ownership of, transactions with, and certain other activities related to controlled foreign partnerships.

Persons To Report Information Regarding Controlled Foreign Partnerships ( Irc Section 6038 ), Transfers To Foreign Partnerships (Irc Section 6038B), And Acquisitions, Dispositions, And Changes In Foreign Partnership Interests ( Irc Section 6046A ).

Persons who have an interest in a foreign partnership. Partners is required to file tax form 8865. Persons with respect to certain foreign partnerships attach to your tax return. Web failure to timely file a form 5471 or form 8865 is generally subject to a $10,000 penalty per information return, plus an additional $10,000 for each month the failure continues, beginning 90 days after the irs notifies the taxpayer of the failure, up to a maximum of $60,000 per return.