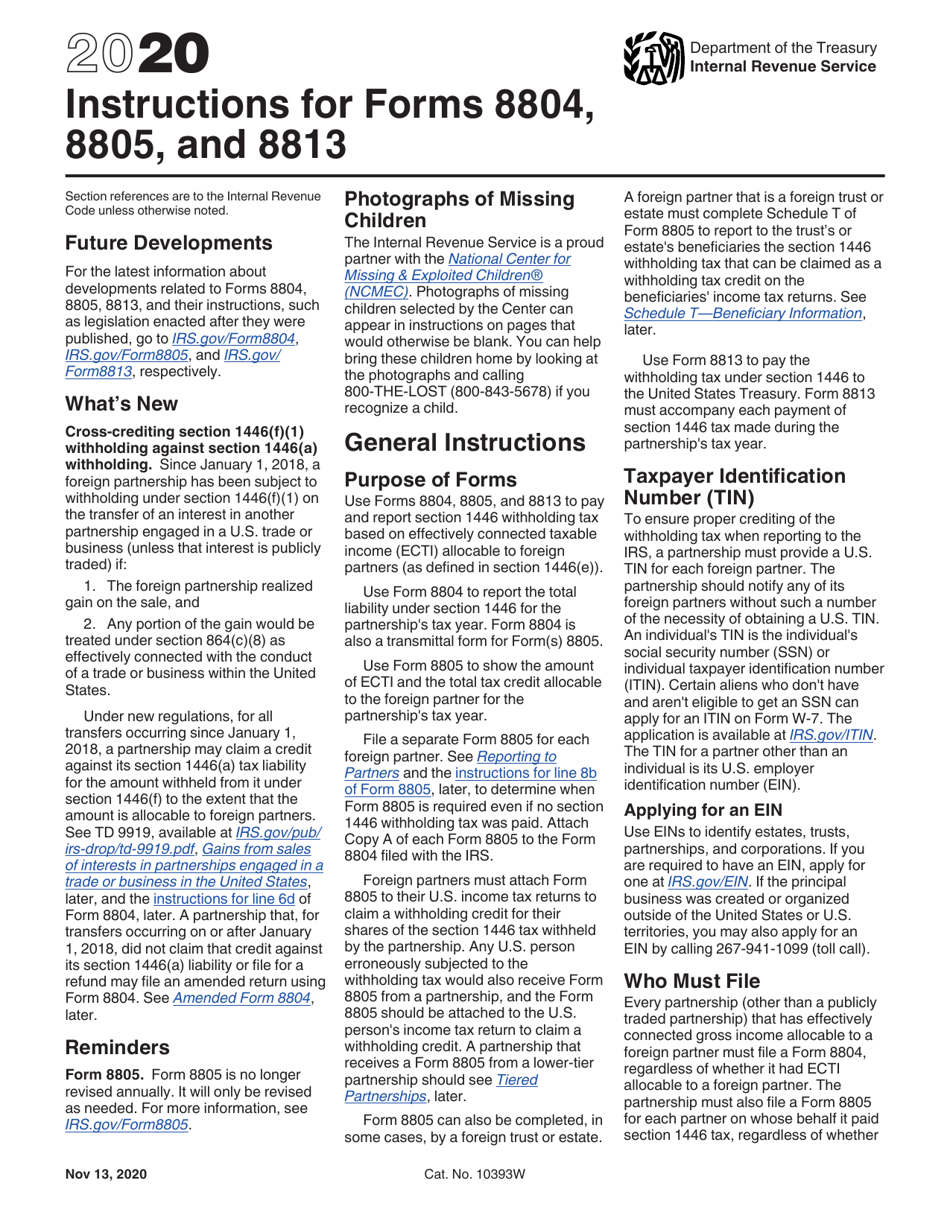

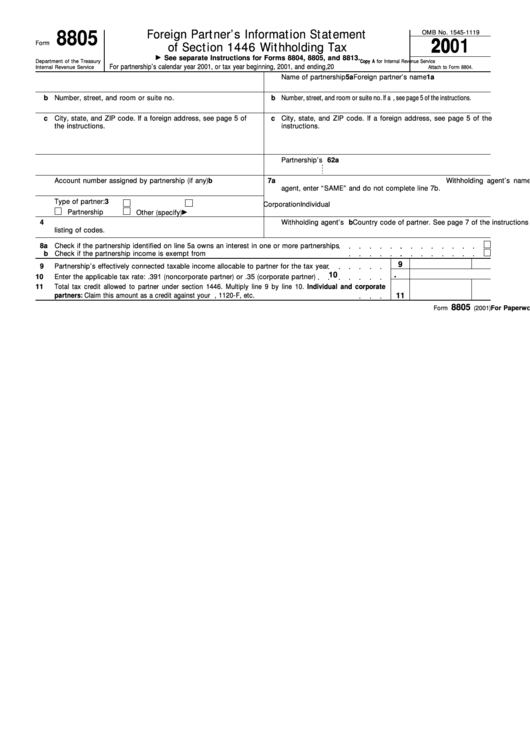

Form 8805 Instructions

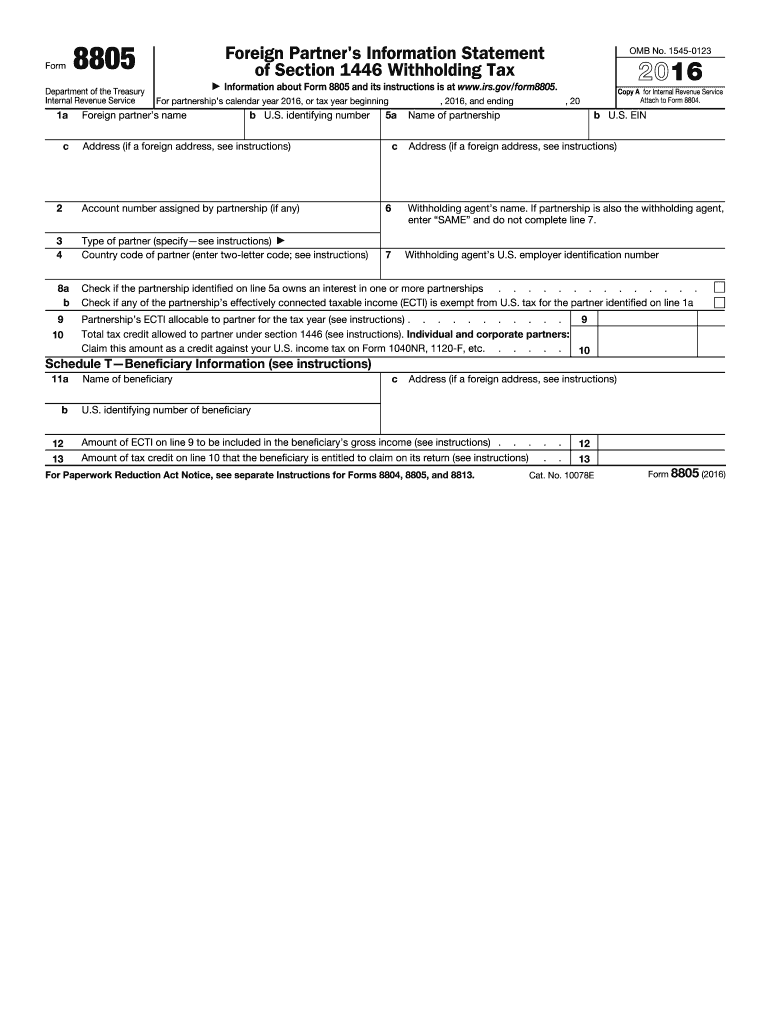

Form 8805 Instructions - The partnership must send a completed copy of this form to all foreign partners involved, even if no withholding tax is paid. File a separate form 8805 for each foreign partner. See reporting to partners and the instructions for line 8b of form 8805, later, to determine when form 8805 is required even if no section 1446 withholding tax was. The partnership must also file a form 8805 for each foreign partner even if no section 1446 withholding tax was paid. This form is used to make payments of withheld tax to the united states treasury. Web we last updated the foreign partner's information statement of section 1446 withholding tax in february 2023, so this is the latest version of form 8805, fully updated for tax year 2022. Web this form is used to show the amount of effectively connected taxable income (ecti) and the total tax credit allocable to the foreign partner for the partnership's tax year. Web form 8805, a foreign partner’s information statement of section 1446 withholding tax is used to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership’s tax year. Trade or business) to report payments of u.s. November 2019) foreign partner’s information statement of section 1446 withholding tax department of the treasury internal revenue service copy a for internal revenue service go to www.irs.gov/form8805 for instructions and the latest information.

Web form 8805, a foreign partner’s information statement of section 1446 withholding tax is used to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership’s tax year. Web this form is used to show the amount of effectively connected taxable income (ecti) and the total tax credit allocable to the foreign partner for the partnership's tax year. The partnership must send a completed copy of this form to all foreign partners involved, even if no withholding tax is paid. Form 8805 reports the amount of eci allocated to a foreign partner. Trade or business) to report payments of u.s. Web a copy of form 8805 must be attached to the foreign partner’s u.s. Web form 8805 is to be filed by a u.s. Web what is form 8805? About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service Web we last updated the foreign partner's information statement of section 1446 withholding tax in february 2023, so this is the latest version of form 8805, fully updated for tax year 2022.

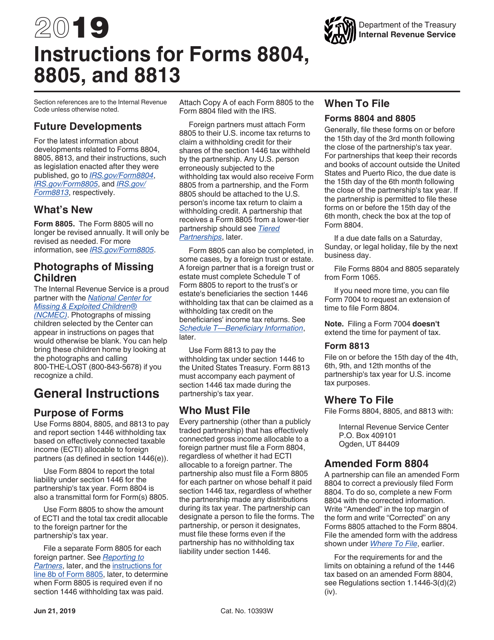

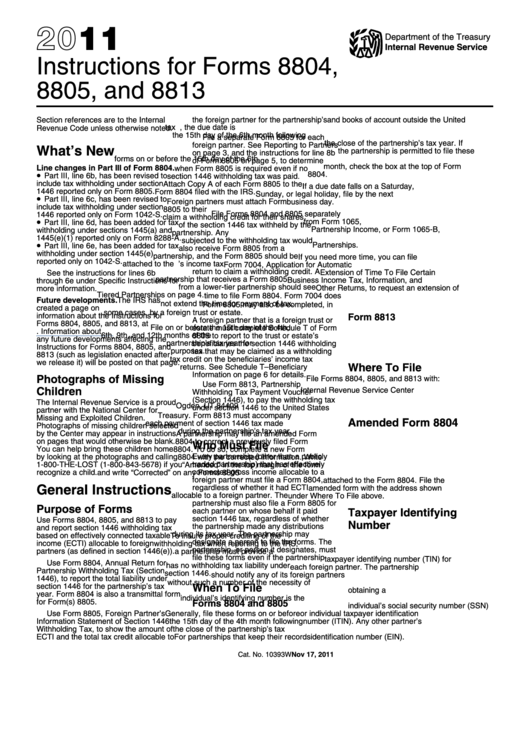

Trade or business) to report payments of u.s. Partnership (or a foreign partnership with effectively connected income to a u.s. Taxes for a foreign partner on the partners' share of the effectively connected income. Web what is form 8805? November 2019) foreign partner’s information statement of section 1446 withholding tax department of the treasury internal revenue service copy a for internal revenue service go to www.irs.gov/form8805 for instructions and the latest information. Web file form 8813 on or before the 15th day of the 4th, 6th, 9th, and 12th months of the partnership's tax year for u.s. The partnership must send a completed copy of this form to all foreign partners involved, even if no withholding tax is paid. Instructions for forms 8804, 8805, and 8813 provides guidance to filers of forms 8804, 8805, and 8813 on how to pay and report section 1446 withholding tax based on effectively connected taxable income. About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service See reporting to partners and the instructions for line 8b of form 8805, later, to determine when form 8805 is required even if no section 1446 withholding tax was.

Form 8802 Instructions 2021 2022 IRS Forms Zrivo

Web this form is used to show the amount of effectively connected taxable income (ecti) and the total tax credit allocable to the foreign partner for the partnership's tax year. Partnership (or a foreign partnership with effectively connected income to a u.s. About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service Form 8805.

Form 8805 Fill Out and Sign Printable PDF Template signNow

Instructions for forms 8804, 8805, and 8813 provides guidance to filers of forms 8804, 8805, and 8813 on how to pay and report section 1446 withholding tax based on effectively connected taxable income. Web we last updated the foreign partner's information statement of section 1446 withholding tax in february 2023, so this is the latest version of form 8805, fully.

Download Instructions for IRS Form 8804, 8805, 8813 PDF, 2020

Web use form 8805 to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership's tax year. Web this form is used to show the amount of effectively connected taxable income (ecti) and the total tax credit allocable to the foreign partner for the partnership's tax year. See reporting to partners and.

Work Sharp Precision Adjust Sharpener Tips & Tricks YouTube

Web form 8805, a foreign partner’s information statement of section 1446 withholding tax is used to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership’s tax year. The partnership must send a completed copy of this form to all foreign partners involved, even if no withholding tax is paid. Taxes for.

Understanding Key Tax Forms What investors need to know about Schedule

November 2019) foreign partner’s information statement of section 1446 withholding tax department of the treasury internal revenue service copy a for internal revenue service go to www.irs.gov/form8805 for instructions and the latest information. File a separate form 8805 for each foreign partner. This form is used to make payments of withheld tax to the united states treasury. Web a copy.

Irs form 8865 instructions

Instructions for forms 8804, 8805, and 8813 provides guidance to filers of forms 8804, 8805, and 8813 on how to pay and report section 1446 withholding tax based on effectively connected taxable income. Web use form 8805 to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership's tax year. Form 8813,.

Download Instructions for IRS Form 8804, 8805, 8813 PDF, 2019

Web form 8805 is to be filed by a u.s. The partnership must also file a form 8805 for each foreign partner even if no section 1446 withholding tax was paid. November 2019) foreign partner’s information statement of section 1446 withholding tax department of the treasury internal revenue service copy a for internal revenue service go to www.irs.gov/form8805 for instructions.

Instructions For Forms 8804, 8805, And 8813 2011 printable pdf download

File a separate form 8805 for each foreign partner. About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service See reporting to partners and the instructions for line 8b of form 8805, later, to determine when form 8805 is required even if no section 1446 withholding tax was. This form is used to make.

Form 8805 Foreign Partner'S Information Statement Of Section 1446

See reporting to partners and the instructions for line 8b of form 8805, later, to determine when form 8805 is required even if no section 1446 withholding tax was. Instructions for forms 8804, 8805, and 8813 provides guidance to filers of forms 8804, 8805, and 8813 on how to pay and report section 1446 withholding tax based on effectively connected.

Form 8805 Foreign Partner's Information Statement of Section 1446

Partnership (or a foreign partnership with effectively connected income to a u.s. About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service Form 8805 reports the amount of eci allocated to a foreign partner. Web file form 8813 on or before the 15th day of the 4th, 6th, 9th, and 12th months of the.

Web A Copy Of Form 8805 Must Be Attached To The Foreign Partner’s U.s.

Form 8805 reports the amount of eci allocated to a foreign partner. The partnership must send a completed copy of this form to all foreign partners involved, even if no withholding tax is paid. Web use form 8805 to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership's tax year. This form is used to make payments of withheld tax to the united states treasury.

Form 8813, Partnership Withholding Tax Payment Voucher (Section 1446).

Web we last updated the foreign partner's information statement of section 1446 withholding tax in february 2023, so this is the latest version of form 8805, fully updated for tax year 2022. Web form 8805, a foreign partner’s information statement of section 1446 withholding tax is used to show the amount of ecti and the total tax credit allocable to the foreign partner for the partnership’s tax year. See reporting to partners and the instructions for line 8b of form 8805, later, to determine when form 8805 is required even if no section 1446 withholding tax was. Trade or business) to report payments of u.s.

November 2019) Foreign Partner’s Information Statement Of Section 1446 Withholding Tax Department Of The Treasury Internal Revenue Service Copy A For Internal Revenue Service Go To Www.irs.gov/Form8805 For Instructions And The Latest Information.

Web form 8805 is to be filed by a u.s. About form 8805, foreign partner's information statement of section 1446 withholding tax | internal revenue service Web what is form 8805? Partnership (or a foreign partnership with effectively connected income to a u.s.

Web This Form Is Used To Show The Amount Of Effectively Connected Taxable Income (Ecti) And The Total Tax Credit Allocable To The Foreign Partner For The Partnership's Tax Year.

The partnership must also file a form 8805 for each foreign partner even if no section 1446 withholding tax was paid. Instructions for forms 8804, 8805, and 8813 provides guidance to filers of forms 8804, 8805, and 8813 on how to pay and report section 1446 withholding tax based on effectively connected taxable income. File a separate form 8805 for each foreign partner. Web file form 8813 on or before the 15th day of the 4th, 6th, 9th, and 12th months of the partnership's tax year for u.s.